“If the 10-year breaks 2.6 percent on a weekly or on a monthly basis, because it’s so strong and so important in terms of technical analysis, that if and when it’s broken on the upside, it’s a bear market,” Gross, who manages the $1.7 billion Janus Global Unconstrained Bond Fund, said Friday in an interview on Bloomberg Television and Bloomberg Radio. “And if it’s not broken on the upside, we just stay where we are.”

Don’t Worry Bond Investors, Baby Boomers Have Got Your Back

by

Natasha Doff

HSBC report sees aging population supporting demand for bonds

Debt already accounts for more than half of pension holdings

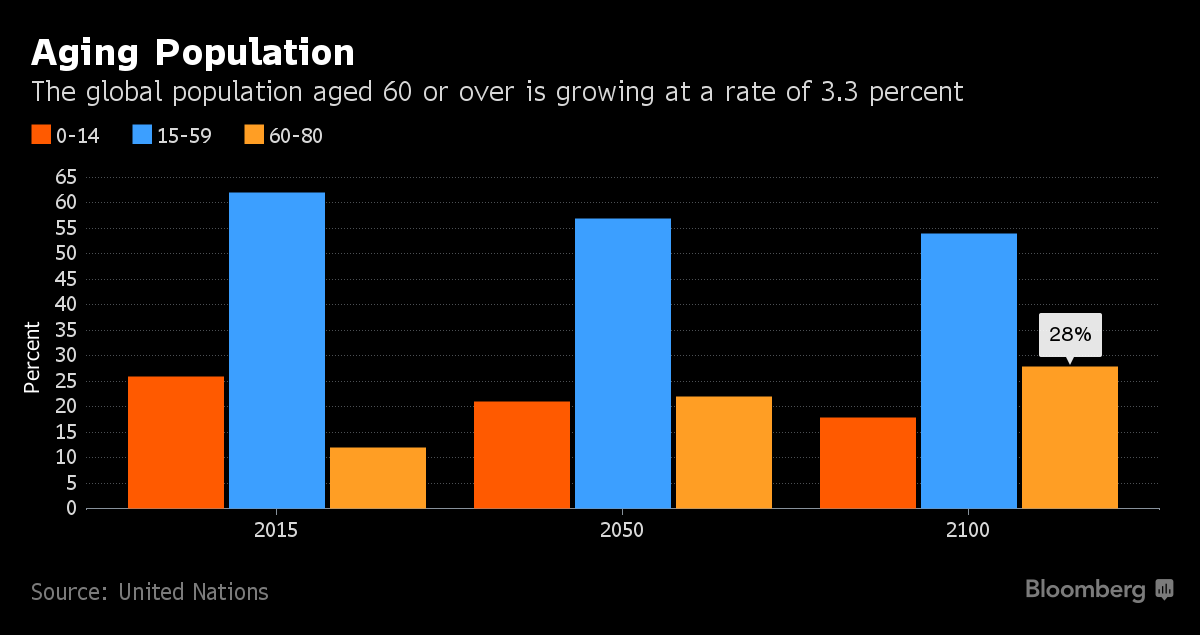

Investors mourning the end of a 30-year bull market in U.S. Treasuries can take solace from demographics: thanks to the aging population there’s a limit to how high yields can go.

Over the next decade, as more of those born in the baby-boom period following World War II get closer to drawing their pensions, global demand for bonds and cash will rise and allocations to equities will fall, according to analysts at HSBC Global Research. That’s because people get more risk averse as they get closer to retirement, shifting out of stocks and into fixed-income investments.

The generation now approaching retirement is both bigger and wealthier than all the other age groups in most of the developed world. So even if cyclical factors such as rising inflation in the U.S. boost the mid-term appeal of stocks over bonds, the longer-term demand for fixed income will remain high, according to Fredrik Nerbrand, global head of asset allocation at HSBC Bank Plc in London.

“If you believe in follow the money, you need to follow the baby boomers,” Nerbrand said in a phone interview. “Bond yields may not revert back to their historical averages even if inflation were to rise because the structural story is still there.”

Tremors in the bond market have renewed interest in an argument that the greying of large portions of developed-market populations will help support bond prices. Jim Leaviss at M&G Investments in London argued in a research note in December that while demographics have helped to push down bond yields in the past, the link has been distorted by factors like government stimulus since the financial crisis and globalization changing the shape of the labor force.

The global population aged 60 or over is growing at a rate of 3.3 percent a year and in Europe, that age group already makes up 24 percent of the total, according to the United Nations 2015 World Population Prospects report. As the ranks of those entering retirement age swell, they are taking a larger slice of the economic pie, with baby boomers in the U.S. now holding more than 45 percent of the total wealth pool, HSBC said in a report.

Pension funds in member states are already allocating more than 50 percent of their holdings to bonds, according to an Organisation for Economic Co-operation and Development study released in June. HSBC forecasts that U.S. allocations to equities will drop by about five percentage points by 2030, offset by a small increase in bond holdings and a larger increase in cash.

That doesn’t mean Nerbrand is betting on bonds in the short term. In the current cycle, with the Federal Reserve set to raise interest rates at a faster pace this year and Donald Trump’s spending plans set to fuel inflation, the place to be is equities, he said.

“There are times when you don’t want to be long bonds from an asset allocation perspective,” Nebrand said. “But generally we would suggest that there is still a structural demand over the next five to 10 years that favors bonds rather than equities.”

* Toronto-Dominion Bank (TD) Aaa/AAA, to price $benchmark

144a/Reg-S 5Y Covered Bond, via managers BMO/BNP/GS/HSBC/TD;

IPT MS +Low-60s

* Added today:

* Kommuninvest (KOMINS) Aaa/AAA, mandates BNP/BAML/Nom/TD

to manage a forthcoming $benchmark 144a/Reg-S 3Y

* Inter-American Development Bank (IADB) Aaa/AAA, mandates

BMO/BAML/HSBC/JPM to lead manage $benchmark Global 5Y

deal

* M&A deals expected in 2017

* Recent updates:

* Empresa de Transporte de Pasajeros Metro S.A. (Metro de

Santiago) (BMETR) na/A+/A, mandates BAML/JPM for

investor calls; 144a/Reg-S 30Y expected to follow

* Fibria Celulose S.A. na/BBB-/BBB-, mandates

BNP/BAML/C/HSBC/JPM for investor meetings from Jan. 6;

10Y Green Bond may follow

* Raizen Fuels Finance na/BBB-/BBB, to hold investor

meeting from Jan.9, via BAML/Bradesco/C/JPM/SANTAN

144a/Reg-S intermediate offering may follow

* PG&E Corp (PCG) Baa1/BBB, filed $350m mixed shelf; last

issued at this level in Feb. 2014

* Republic of Korea (KOREA) Aa2/AA, mandates

BAML/C/GS/HSBC/KDB/Samsung for investor meetings Jan.

9-11; USD deal may follow

* Has not priced a new USD issue since June 2014

* Apple (AAPL) Aa1/AA+, added as possible early 2017

issuers based on history

* United Technologies (UTX) A3/A-, said in Dec. 14

guidance call it will tap the debt markets in early 2017

to complete its share buyback program

* 3M (MMM) A1/AA-, plans to add up to $2.8b of debt in

2017, suggesting another yr of incrementally higher

leverage: BI

MANDATES/MEETINGS

* Scentre Group (SCGAU) A1/A; mtgs Dec. 5-8

* ACWA Power; mtgs from Nov. 23

* Adani Ports (ADSEZ) Baa3/BBB-; mtgs from Nov. 13

* Korea Hydro & Nuclear Power (KOHNPW) Aa2/AA; mtgs Oct. 18-20

SHELF FILINGS

* Mercury General (MCY) files debt shelf; last seen in 2001

* Puget Sound Energy (PSD) A2/A-; $800m debt shelf (Nov. 8)

* Dow Chemical (DOW) Baa2/BBB; debt shelf; last issued in

Sept. 2014 (Oct. 28)

* Darden Restaurants (DRI) Baa3/BBB; debt shelf, last seen in

2012 (Oct. 6)

* Western Union (WU) Baa2/BBB; debt shelf; last issued Nov.

2013 following Oct. 2013 filing (Oct. 3)

OTHER

* European Stability Mechanism (ESM) Aa1/–; mandates for

advisement on inaugural USD issuance (Oct. 21)

* ConAgra (CAG) Baa2/BBB-; could borrow up to $2.5b for

acquisitions, BI says (Oct. 19)

Posted in Uncategorized | Comments Off on Corporate Bond Pipeline

The prime minister said the U.K. would aim for a clean break from the EU

By

Mike Bird

The pound fell sharply against the dollar and euro Monday after U.K. Prime Minister Theresa May said Britain would make a definitive break from the European Union.

The pound fell 1.23% to $1.214 against the greenback, taking sterling to the levels it traded at in October. It was down 1.11% against the euro at €1.154. Sterling was as high as $1.24 Thursday.

On Sunday, Ms. May said in an interview with Sky News that the U.K. would aim for a clean break from the EU, reiterating her intention for Britain to negotiate control over immigration in upcoming Brexit negotiations.

“Often people talk in terms as if somehow we are leaving the EU, but we still want to kind of keep bits of membership of the EU,” Mrs. May said in an interview with Sky News.

“We are leaving. We are coming out,” she added, saying that the U.K. still wanted the “best possible deal” in terms of trade.

The EU’s 27 other heads of government have said that freedom of movement for EU citizens is a requirement for access to the bloc’s single market, with is the biggest destination for British exports.

On Monday, a spokeswoman for Mrs. May said the Prime Minister hadn’t ruled anything out or in.

”She’s said she wants the best possible deal for trading with and operating within the single market,” the spokeswoman said.

Though U.K. economic data has surprised on the upside, many analysts believe the pound will continue to head lower.

Sterling is also being hit by the strong dollar, which has gained in recent months on a belief that the U.S. Federal Reserve will raise interest rates at a faster rate in 2017. The WSJ Dollar Index was up 0.24% Monday.

Morgan Stanley sees sterling falling to $1.17 this quarter, because it thinks political uncertainty will impact investment in 2017.

However, some forecasters disagree.

“We think further signs that the government is being forced toward a soft Brexit will emerge, enabling sterling to climb back to about $1.30 and €1.24 by the end of this year,” Samuel Tombs, chief U.K. economist at Pantheon Macroeconomics, said in a research note.

US retail sales late in the week is the main data feature this week

The short squeeze in the Chinese yuan appears to have ended

UK Prime Minister May comments suggest hard Brexit, which weighs on sterling

Brazil is expected to cut 50 bp in the Selic rate this week

May’ weekend comments indicated a willingness and strategic thrust to abandon the single market in exchange for regaining control over immigration and not being subject the European Court of Justice sent sterling off more than 1% today to lead the major currencies lower. The Australian and New Zealand dollar’s are slightly firmer, withe most of the other currencies little changed. Japanese markets were closed for a national holiday, and the dollar is straddling the JPY117 area. Germany reported a larger than expected jump in November exports (3.9%, best in more than four years), but did little for the year which stalled near $1.0555 only to slip toward $1.05 in the European morning. Equities are mostly lower, thought the currency-sensitive FTSE 100 extended its winning streak into a tenth session. Bonds a recovering following the sell-off before the weekend, with Italian and Spanish 10-year yields seven basis points lower and German yield a single basis point lower. The yield on 10-year Treasuries is 2.5 bp lower to push slightly through 2.40%. Lastly, we note that the South Korean won is more than 1% lower as a dispute with Japan led to the suspension of discussions about a swap line and North Korea threatens the launch of a long-range missile.

The major US equity indices reached record highs before the weekend even if the Dow 20000 level was just out of reach. Following news of a stronger than expected rise in hourly earnings, US yields rose, and after an initial stumble, the dollar recovered on closed on its highs.

The underlying narrative that explains and justifies these broad trends stands on four legs. First, that the US economy is expanding at a sufficient clip to spur some price pressures, including, as we saw in the employment report, hourly earnings. (2.9% year-over-year, a new cyclical high, though below past recoveries and expansion levels). Second, that the economic policies of the new Administration will be pro-growth in the form of de-regulation, tax changes, and nationalist economic policies. Third, that other high income countries are expanding at least near-trend, and price pressures appear to have bottomed. Fourth, populist-nationalist forces will be featured on the European political stage, posing the last expression of the existential threat.

The headwinds on the US economy abated in the middle of last year. The economy expanded at a 3.5% annualized rate in Q3 16 and, while it likely slowed, with less of a contribution from consumption, and a drag from net exports, recent data prompted upward revisions to the Atlanta Fed GDP tracker to 2.9% for Q4. The Bloomberg consensus is 2.3%, while the NY Fed’s tracker has it at 1.9%. Some economists are suggesting there is better than a one in three chance of a Fed hike in March, while the CME estimates that the Fed funds futures currently discounts about a one in four chance.

The December retail sales data that will be reported on January 13 will give no reason to doubt basic scenario. The headline may be flattered by the better than expected vehicle sales and the increase in gasoline prices. The GDP should rise around 0.3%, consistent with consumption rising at a slightly than the 3.0% pace in Q3.

In Europe, the main feature is November industrial output reports. Industrial output in the UK and eurozone is expected to have risen by 0.5%-0.6%. The main difference is in year-over-year pace. The eurozone’s pace may more than double from the 0.6% clip seen in October. The UK’s industrial output my turn positive (~0.5%) after contracting (-1.1%) in October.

Separately the UK reports the November trade figures. The UK deficit is expected to widen out toward GBP3.5 bln from just below GBP2 bln in October. The average monthly shortfall this year has been GBP3.44 bln vs. GBP2.66 bln in 2015. Also, Sweden and Norway report CPI. Sweden, where the central bank is still pursuing very aggressive unorthodox monetary policy is likely to see a further rise in inflation. It is expected to rise 0.4%-0.5% on the month for a 1.6% year-over-year pace, the fastest in four years. Even with a 0.1% decline in the Norway’s monthly consumer prices, the year-over-year rate may still rise to 3.8% from 3.5%.

Japan reports its November balance of payments. It typically deteriorates in November compared with October. This has been the case without exception since 2006. Before then, it had often improved. Many observers focus the yen’s impact through the trade channel, but given Japan’s large holdings of foreign assets, the pullback in the yen will boost the investment income balance, arguably more directly than the trade balance.

In 2015 and early 2016, Chinese developments rattled the investors; now considerably less so. However, the powerful short squeeze engineered by PBOC officials does not appear aimed at reversing the yuan’s decline as much creating a powerful disincentive for speculators to think it is a one-way bet. In the larger picture, the same fundamental considerations that we think will underpin the dollar against the major and emerging market currencies are at work with the yuan as well. That means that we expect the yuan to move lower on a trend basis.

Nevertheless, the near-term outlook is a bit of cat-and-mouse with Chinese officials and how persistent it wants to be. As painful as it was for some players last week, the second that officials appeared to back off, they jumped right back into the fray. On Monday the money market rates eased and the yuan, especially the offshore variant fell.

China reported that reserves fell by a little more than $41 bln in December to $3.01 trillion. It is the smallest in decline in three months, and in line with market expectations. Interestingly, the debate about China’s reserves has transformed from it having too much to wondering if it has a sufficient level of reserves. Also, because the opaqueness of China’s intervention, in the derivatives market or forward market, forward market, for example, more reserves may be encumbered (committed).

China is expected to report inflation figures and the December trade surplus. China’s CPI has gradually firmed. The 24-month average in November was 1.7%, while the 12-month average 2.0% and the three-month average may tick up to 2.2% in December. It is the PPI that is surging. Recall it was negative (deflationary) for five years through late Q3 16. After turning positive in September (0.1%) it jumped to 1.2% in October and 3.3% in November. It is expected to rise toward 4.6% in December. Often when producer prices rise faster than consumer prices, investors get concerned about profit margins. Some economists also talk about pipeline inflation, but this seems to be more an exception than the rule.

China’s trade surplus is expected to edge toward $47.5 bln from $44.6 bln in November. Exports likely deteriorated after edging 0.1% higher year-over-year in November. The improvement likely stems from a slowing in imports. China’s monthly trade surplus is fairly stable. The three, 12, and 24-month averages converge between $44.3 and $46.5 bln. Separately China may also report that credit expansion slow, but remains elevated. Consider that this year’s monthly average of aggregate social financing is CNY1.46 trillion compared with CNY1.27 in 2015.

Brazil’s central bank began its easing cycle last October and had a follow-up rate cut in November. The consensus calls for a 50 bp cut in the 13.75% Selic rate. The US dollar has been trending lower against the real since early December and by the end of last week had returned to near where it was trading before the US election. We suspect the move is exhausted or nearly so. Just as a year ago, the market may have exaggerated the negatives, it seems that the positives may be exaggerated now. The dollar finished last week near BRL3.2225. We see risk in the coming week or two toward BRL3.30.

Lastly, we note three political issues that may become talking points in the days ahead. First, the tensions between Greece and the EU has eased since the middle of December, and a new tranche of aid is expected shortly. Greece’s 10-year bond yield fell 25 bp last week to bring the decline to about 45 bp since Christmas Eve. Note that investors will likely learn in the days ahead that Greece is still experiencing deflation. Greece will also report November industrial output (6.8% year-over-year in October) and October unemployment (23.1% in September). Meanwhile, Greece’s privatization efforts appear to be progressing with the sale of a 51% stake in the Piraeus ports to a Chinese company while has been managing a couple of piers.

Second, a decision by the UK Supreme Court on the royal prerogative regarding triggering Article 50 to begin the formal negotiations for leaving the EU is expected over the next couple of weeks. Prime Minister May confirmed two things many investors have suspects: that there were not plans for Brexit before the referendum and that the UK will leave the single market. This may weigh on sterling, which lost more than 1% before the weekend to fall for the fourth week in the past five. Separately, we note that a 24-hour London Underground strike will make for difficult commutes on Monday.

Third, the US Senate is set to begin taking up the President-elect’s nominations. Although it is widely recognized Presidents’ prerogative to pick their own advisers and cabinet, many of the nominees are particularly contentious for Democrats, and some Republicans may challenge a couple of the nominees as well. The process begins in earnest with a Senator Sessions (Republican from Alabama) nomination for Attorney General. Sessions’ views on civil rights, including voting rights, same-sex marriage, and immigration, as well as Trump’s proposal to establishing a registry of Muslims and imposing a ban on their immigration, will make for a particularly heated hearing.

Investors Betting Strongest Junk-Bond Rally in Years Has Legs

Better earnings among risky companies and a slowdown of defaults have given junk-bond investors cause for optimism despite a big decline in yields

An uptick in earnings among riskier U.S. companies is bolstering investor confidence that an epic rally in junk bonds can last a little longer.

After six straight quarters of year-over-year declines, earnings of low-rated companies increased 14% in the second quarter and 72% in the third quarter, according to Bank of America Merrill Lynch. At the same time, defaults slowed following a wave of bankruptcies in the energy sector.

Because of those factors, some investors and analysts say junk bonds— issued by companies that are often small and burdened by debt—could do much better than might be expected after such a strong year.

“From my vantage point, fundamentals are the most important thing” and “they’ve modestly improved,” said Michael Contopoulos, head of high-yield strategy at Bank of America, noting stronger earnings and steady oil prices have reduced risks.

The average junk bond yield was 5.86% Thursday, a two-year low but above the sub-5% levels it reached in 2014. Despite the low yields, many investors still view junk bonds as attractive at a time when the 10-year Treasury note yield is below 2.5% and stock valuations are widely seen as inflated.

Among the many junk-rated companies that had better earnings was Sprint Corp., which reported a 17% increase in adjusted earnings before interest, taxes, depreciation and amortization in the quarter ended Sept. 30 from a year earlier. Its 7.625% bonds due 2025 last traded at around 107 cents on the dollar, up from 75 cents on the dollar in June, according to MarketAxess.

The Bloomberg Barclays U.S. Corporate High Yield Index returned 17.1% in 2016. That was its best total return since 2009 and better than those produced by all three major stock indexes, as well as investment-grade corporate bonds and U.S. Treasurys.

Such a performance almost certainly can’t be replicated in 2017. Unlike stocks, there is a limit to how much bonds can rally because they mature at 100 cents on the dollar.

As bond prices rise, their yields decline. Before last year, junk bonds had produced double-digit returns four times in the previous 10 years and each time returns were much lower the following year.

Still, many investors and analysts are fairly optimistic about how junk bonds will perform.

Of six large banks surveyed by The Wall Street Journal, four project positive returns for junk bonds in 2017. J.P. Morgan Chase & Co. is the most bullish, predicting an 8% return. Wells Fargo & Co. is projecting 5% to 6%, while Bank of America Merrill Lynch is estimating 4% to 5% and Goldman Sachs Group Inc. is expecting 3.2%.

“High yield is a pretty resilient asset class,” said John McClain, a high-yield bond portfolio manager at Diamond Hill Capital Management in Columbus, Ohio. Though the market hit a rough patch in early 2016 as recession fears increased and sellers had trouble finding buyers, “that got fixed very quickly,” he added.

Of course, junk bonds still face risks. They are especially sensitive to economic downturns, sometimes picking up signs of stress before the stock market.

Though they aren’t as vulnerable to rising Treasury yields as investment-grade corporate bonds, junk bonds likely would decline in price if the Federal Reserve raises interest rates more quickly than expected and government bond yields increase sharply. That is especially true for higher-rated bonds with lower yields.

One wild card is the volume of new bonds added to the market. While bond sales tend to drop off during times of market stress, robust issuance can also depress prices of outstanding debt due to supply-demand dynamics.

Unlike the investment grade bonds, which set a record for issuance in 2015 and nearly matched that total last year, the volume of new high-yield bonds has declined in recent years, totaling $261 billion in 2016 compared with $269 billion in 2015 and a record $359 billion in 2013, according to Dealogic.

Posted in Uncategorized | Comments Off on Can the Epic Junk Bond Rally Continue?

As Dow Approaches 20000: Has This Rally Just Begun?

As some investors consider swapping out of bonds, analysts see a tailwind for stocks

By

COLIN BARR and

AARON KURILOFF

Perhaps this rally hasn’t ended. Perhaps it has just begun.

The Dow Jones Industrial Average on Friday closed at 19963.80, as it nears 20000 and extends an upswing that began in the depths of the financial crisis. When it arrives at 20000, it will be the Dow’s 14th thousand-point milestone since then and the second-fastest on record.

The stock rally ranks among the least-beloved in history, traders and analysts say. The technology bust and the financial meltdown taught individuals to shy away from stocks and to embrace bonds and cash. Investors poured $381 billion into bond mutual and exchange-traded funds between the start of 2014 and October, according to EPFR Global. Over the same span, they pulled a net $16 billion from stock funds.

It is a strategy that many have pursued to their detriment. The Dow has returned 274%, including price gains and dividends, since its 2009 bottom. The 10-yearU.S. Treasury note has returned 33% over the same span. Now, with many on Wall Street raising their estimates for U.S. economic growth in coming years following the surprise election of Donald Trump, swapping out of bonds for stocks is an idea that is coming up more in conversation.

“People are saying, is it safe to get in now” to the stock market, said James D. McDonald, chief investment strategist at Northern Trust Corp. in Chicago, with $946 billion in assets under management.

Some analysts view this underinvestment as a tailwind for stocks, which they also contend look relatively attractive to many other investments based on measures such as corporate earnings, dividend yields and the economic outlook. While the U.S. economic expansion already ranks among the longest on record, few see signs that a slowdown is imminent. And if investors gain confidence, they could pour money into stocks and drive major indexes still higher.

For now, “people still feel the market going up is temporary and speculative,” said Richard Bernstein, chief executive of Richard Bernstein Advisors, a New York investment adviser with $3.1 billion in assets under management.

Roughly 46% of investors were bullish as of Jan. 4, according to the weekly survey by the American Association of Individual Investors. That is above the long-term average of 38% but far below the peaks of 75% reached in January 2000 and 58% in 2007. Investors often use the survey as a contrarian indicator, selling when bullish sentiment reaches highs and buying when bearishness spikes.

One investor who embodies these conflicting impulses is Al Tomei, a 75-year-old from Los Angeles who retired as a facilities planner for the Los Angeles Unified School District.

He maintained a split portfolio of half bonds and half stocks as recently as 2007, when the Dow peaked above 14000 before losing more than half its value in the financial crisis. The Dow lost 32% on a total-return basis in 2008.

Since then, Mr. Tomei has kept about 80% of his portfolio in bonds. He is now thinking about moving back toward a 50-50 split, concerned that Mr. Trump’s plans to increase fiscal spending and cut taxes will boost inflation, chipping away at the value of bonds’ fixed payments. The Dow’s total return was 16% in 2016, roughly half of that since Mr. Trump’s Nov. 8 election.

Mr. Tomei worries that stocks are due for a correction after the gains of the past year, which he views as being fueled by external factors such as stock buybacks and central- bank stimulus rather than fundamental improvements in the U.S. economy. He is holding 4% to 5% of his assets in cash for now and looking for opportunities to buy stocks cheap.

“Everything I’ve read is that stocks are richly priced and when they’re richly priced, the odds of them going higher are not particularly good,” said Mr. Tomei.

Valuations are indeed stretched relative to history, said Messrs. Bernstein and McDonald. Stocks in the S&P 500 traded Thursday at roughly 21 times their past 12 months of earnings, up from a 10-year average of 16, according to FactSet. But they say the valuations aren’t extreme given how low interest rates remain relative to history, a condition that tends to push investors into stocks as a higher-yielding alternative, while keeping borrowing costs low for companies.

Bond yields have surged by more than a percentage point since hitting all-time lows this past summer, with the 10-year Treasury yield rising to 2.417% on Friday.

The dividend yield on the S&P 500 was roughly 2% Friday, according to S&P Dow Jones Indices. That makes stocks competitive with bonds as a source of income, while offering greater potential for asset appreciation, several investors said.

Other metrics look relatively good for stocks as well. Corporate earnings, a major driver of stock-price gains over time, have begun rising after a sharp decline during the 2014-2016 energy bust. Strong earnings growth can mitigate valuation concerns, Mr. Bernstein said. Analysts expect S&P 500 earnings to rise 11% from a year ago in the first quarter, according to FactSet.

Mr. Bernstein said his firm began buying cyclical stocks such as energy, materials, technology and financial firms in the first quarter of 2016, when market-based inflation expectations began rising. He said Mr. Trump’s promise of fiscal stimulus “creates an almost unprecedented” stockpile of fuel for further stock gains. Stimulus plans typically are enacted at an earlier stage of the economic cycle when unemployment is higher. Mr. Bernstein said: “4.7% joblessness plus fiscal stimulus—whoa! That hasn’t happened in my career.”

Mr. McDonald of Northern Trust said he saw signs of improving global growth starting in May, when purchasing managers’ reports began showing signs of renewed strength.

His firm sharply increased its stockholdings after Mr. Trump was elected in November. Mr. McDonald said he believed Republican control of Congress would enable the new administration to play a more constructive role in facilitating economic growth than has happened in years of mostly divided government. He also said he believes the election has had a confidence-boosting effect throughout the economy.

Yet some remain unconvinced, scarred by the financial crisis and concerned that both stocks and bonds remain expensive. Many investors are holding cash, “waiting for the market to fall or worried about investing because they believe prices are too high,” said Eric D. Nelson, managing principal at Servo Wealth Management, an investment adviser in Oklahoma City. “Honestly, I can’t remember the last time I encountered an investor who is fully invested.”

Summers Warns of Financial-Crisis Risk From Trump Economic Plans

by

Christopher Condon

Financial deregulation would be ‘hugely dangerous,’ he says

Ex-Obama adviser says stronger dollar would hurt exporters

Former U.S. Treasury Secretary Lawrence Summers attacked the policy proposals of Donald Trump on several fronts, saying the president-elect’s plans for deregulation were setting the stage for the next financial crisis.

“The deregulation in some areas like finance is hugely dangerous,” Summers said Sunday in an interview on Fox News Channel. “Who wants to go back to the era of predatory lending? Who wants to go back to the era of vastly over-levered banks?”

Members of Trump’s transition team have vowed to dismantle the 2010 Dodd-Frank Act, the principal legislative response to the 2008-09 global financial crisis, although Trump himself has given mixed signals on Wall Street regulation. During his campaign, he railed against Dodd-Frank, which greatly increased restrictions on banks operating in the U.S., but also said he would reinstate a separation between bank lending and securities underwriting, which was removed in 1999.Summers, former chief economic adviser to President Barack Obama and Treasury secretary under President Bill Clinton, also took aim at Trump’s protectionist rhetoric. That’s already caused a plunge in the Mexican peso, giving Mexican manufacturing an extra advantage over U.S. competitors.

Jawboning Automakers

“Every business deciding whether to locate in Ohio or Mexico is finding Mexico 20 percent cheaper,” said Summers, who’s now a Harvard University professor. “That’s a huge tilt against the United States.”

The peso has lost 14 percent against the dollar since the Nov. 8 election.

Trump, via Twitter, has jawboned a number of companies, including automakers General Motors Co. and Toyota Motor Corp., on their plans for expansion in Mexico. “Toyota Motor said will build a new plant in Baja, Mexico, to build Corolla cars for U.S. NO WAY! Build plant in U.S. or pay big border tax,” Trump said in a Twitter post on Jan. 5.

Trump’s plans to reduce corporate taxation, Summers said, would “hugely increase inequality” and could also help strengthen the dollar, further hurting U.S. exporters and the people who work for them.

While Summers favors a big increase in infrastructure spending in the U.S. as a way to boost productivity and growth, he called Trump’s plans on that front “a Potemkin village of nothing.”

Trump’s proposal called for filling an estimated $1 trillion “10-year funding gap” of spending on bridges, highways and airports through private investment and tax credits. Prospects for the plan in Congress among Republican lawmakers are unclear.

Posted in Uncategorized | Comments Off on Summers on Trump’s Economics

BofA Said to Boost Bonuses for Bond Traders, Cut Equities

by

Laura J Keller

and

Hugh Son

Fixed-income staff to get as much as 10% more for 2016

Equities slump prompts cut of about 5% for that bonus pool

BofA Said to Boost Bonuses for Bond Traders

Bank of America Corp. is poised to boost bonuses for many of its bond traders and trim payouts for those handling stocks, people with knowledge of the matter said. The combined compensation pool will drop significantly, though fewer workers will divvy the rewards.

Senior executives have earmarked as much as 10 percent more to pay the fixed-income division’s staff for 2016 after weighing the impact of fewer employees, the people said, asking not to be identified because the decisions are private. The bank carved out about 5 percent less for equities traders after that business slowed. Individual trader’s payouts could vary from those figures, depending on which products they handle.

Fixed-income operations that struggled for years sprang back to life in the second half of 2016, prompting good news on that front for bonuses. Even as revenue rises in some operations, Bank of America cut so many people during the slump that personnel costs are lower. That’s allowed the bank to reduce the overall compensation pool for the trading and sales operation from a year earlier, the people said.

“We have less people going through our bonus pools,” Chief Executive Officer Brian Moynihan told investors on a conference call in October. “Comp continues to drift down” in a number of Wall Street businesses, he said.

Pay changes may vary widely by region. Workers in Asia and Europe may see their compensation fall by a larger percentage than in the U.S., the people said.

A spokeswoman for the Charlotte, North Carolina-based bank declined to comment on the bonus figures.

Many fixed-income desks saw revenue climb after the U.K.’s June vote to leave the European Union roiled government bond and currency markets and sparked client trading. In November, Donald Trump’s surprise U.S. election win sent shares of investment banks soaring as investors anticipated another trading jolt and an easing of regulations that have reined in risk-taking and made certain transactions more expensive.The fixed-income revival contrasts with banks’ equities businesses, where fees reaped from trading have been dwindling as stock issuance wanes. Morgan Stanley, Wall Street’s biggest stock-trading firm by revenue, is cutting its global bonus pool for the equities division by as much as 4 percent, people with knowledge of the plans said this week.

Posted in Uncategorized | Comments Off on Fixed Income Bonus Time

Potential Fed Chairs Suggest They Would Pursue Tighter Policy

by

Rich Miller

Bank is behind curve in raising rates, Stanford’s Taylor says

Hubbard, Warsh also point toward higher interest rates

Potential candidates to head the Federal Reserve in 2018 suggested that monetary policy would be tighter if they were in charge.

Speaking at the annual American Economic Association meeting that ended Sunday, Glenn Hubbard of Columbia University, along with Stanford University’s John Taylor and Kevin Warsh, criticized the central bank for trying to do too much to help an economy struggling with problems that monetary policy can’t solve.

John Taylor

Photographer: Andrew Harrer/Bloomberg

Fed watchers see the three, all former officials in George W. Bush’s administration, as among the candidates to take over should President-elect Donald Trump decide not to nominate Janet Yellen for another four-year term as chair when her current one expires in February 2018. Trump criticized Yellen during his successful campaign for the White House, at one point accusing her of keeping interest rates low to benefit the Democrats.

“The Federal Reserve is a little behind the curve” in raising interest rates, Taylor, a Treasury undersecretary for international affairs under the last Republican president, said Saturday during a panel discussion in Chicago.

Hubbard, who headed the Council of Economic Advisers under Bush, said he agreed with what he perceives as Trump’s stance that the U.S. has depended too much on the Fed to support the economy in recent years.

Dated Policy

“The Federal Reserve was very successful in the initial period after the crisis but continued a policy perhaps past its shelf life,” he said during an economic association panel on which he appeared with Taylor.

The Fed raised interest rates in December for the second time since 2006 as part of a process known as normalization, after holding them near zero for seven years. Its target for the overnight interbank federal funds rate is now 0.5 to 0.75 percent. Policy makers expect to increase the range’s midpoint to 1.4 percent by the end of 2017 and 2.1 percent by the end of 2018, according to the median of their projections released on Dec. 14.

Hubbard said the Fed might accelerate its rate hikes if Trump looks like he’ll succeed in pushing through his plan for big tax cuts and increased outlays on infrastructure.

“One would expect that the normalization that the Fed was already engaged in will continue at perhaps a more brisk pace,” Hubbard said.

Glenn Hubbard

Photographer: David Paul Morris/Bloomberg

But he said the central bank shouldn’t rush any response and instead should take a “wait and see” approach so it can better judge the impact of whatever measures the president-elect and the Republican-led Congress look set to agree on.

“There’s a difference between policy actions that are likely to lead to overheating — an underfunded infrastructure bill comes to mind — versus policy changes that affect the supply side and productivity,” Hubbard said. “We don’t know yet which” it will be.

The dean of Columbia University’s Graduate School of Business reckons that Trump’s budget and deregulation plans could lift annual economic growth to 2.75 percent in coming years, from about 2.1 percent during the expansion that began in 2009.

Other policies not yet articulated would be needed to boost it higher, according to Hubbard. Trump himself has said he wants to raise growth to 3.5 percent annually.

Hubbard cautioned the incoming administration against making “aggressive” assumptions in its budget about the economic impact of its tax reforms that don’t take account of the Fed’s likely response to them.

Warsh’s Views

Speaking at a different economic association panel on Friday, Warsh, a former Fed governor and Bush economic adviser, said that the composition of the eventual fiscal measures would be more important than their size in assessing their impact.

Kevin Warsh

Photographer: Chris Ratcliffe/Bloomberg

He was skeptical, though, that the Fed’s computer modeling of the economy was up to the task of making that analysis.

Warsh argued that the Fed missed opportunities earlier in the economic expansion to raise rates by pursuing what he called a “ride-the-wind” policy that was too short-term focused.

He questioned why rates are so low when the Fed is so close to achieving its goals of maximum employment and price stability. “Tell me again why interest rates seem to be so far away” from what is at least the historical target, Warsh said.

Warsh concentrated his comments on a call for widespread reform of the central bank. The Fed needs to take better account of the financial cycle in conducting monetary policy — the ups and downs of money, finance and credit, according to the lecturer at the Stanford Graduate School of Business.

He also argued that it should stop relying so much on the “latest noise” from incoming data and instead set out a “well-defined, well-articulated strategy” for meeting its goals.

Taylor Rule

Taylor also called for changes at the Fed and repeated his support for Republican lawmakers’ efforts to get the central bank to adopt a rule to guide monetary policy.

The Stanford professor, who is known for developing his own policy rule, said such a step would make the Fed’s actions more predictable.

“We need some monetary reform,” Taylor said, adding, “Personnel is part of that.”

Two of Trump’s cabinet picks have offered at least guarded praise of Yellen. Treasury nominee Steven Mnuchin said Nov. 30 that the Fed chair has done a “good job,” and Commerce pick Wilbur Ross said she did a “reasonably good job” with a difficult situation.

Posted in Uncategorized | Comments Off on Musings and Ruminationsof Prospective Trump Fed Chairs